Of the index’s 18 components, seven are measures of interest rates (Fed Funds, Treasuries, corporate bonds, and asset backed securities), six are measures of yield spreads, and five “Other Indicators” are a grab bag of measures that include the VIX volatility index, expected inflation rate (10-year Treasury yield minus 10-year TIPS yield), and the S&P 500 Financials index.

The components – except for the Fed Funds rate – are measures of how market participants perceive financial stress, and how they react to it. In bubble times, when exuberance rules the day, and when nothing can go wrong, and when risk has been banished from the system, and when interest rates are low, perceived financial stress disappears.

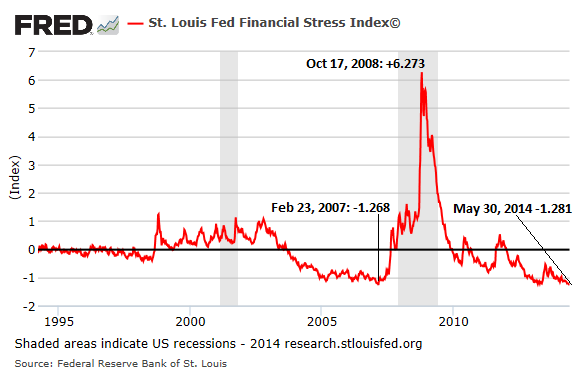

But the gauge is a horrible predictor. So horrible that it has become a contrarian indicator. The prior record low of “financial stress” was achieved when the financial system in the US was in the early stages of collapsing under mountains of toxic securities and mega-bets put together and sold at peak valuations to conservative-sounding funds held by unsuspecting investors in their retirement nest eggs. And banks stuffed them into their basements and into off-balance sheet vehicles, and their financial statements spoke of values and profits that didn’t exist, and no one cared. Greed ruled the day. Damn the torpedoes, full speed ahead.

It isn’t that low financial stress caused the Financial Crisis. It’s that low financial stress incited decision makers – from homebuyers to bank CEOs – to make willfully reckless decisions that can only be made and funded when there is money for everything, and when this crap can be unloaded no questions asked. It happened in 2007, and it’s happening now again.

No comments:

Post a Comment