http://gold-stater.com is now providing daily gold market and gold coin market commentary and updates. Please check in regularly to find the latest developments in gold and gold coins.

American bankers who brought on the 2008 global financial collapse,

by and large, didn’t get indicted, or face any significant consequences

for their actions. In fact, many of them even got huge bonuses.

That wouldn’t have been the case in Vietnam, another nation struggling with corrupt and unscrupulous bankers.

During a recent cleanup of Vietnam’s financial sector, the strictly

authoritarian nation sentenced three bankers to death by firing squad in

the past six months alone.

A pair currently on death row had embezzled roughly $25 million from

the state-owned Vietnam Agribank. Back in March, a 57-year-old former

regional boss from Vietnam Development Bank, found himself sentenced to

death by firing squad over a $93-million swindling job.

According to Vietnam’s Tuoi Tre news outlet, many of the

co-conspirators got life in prison, with the “Madoffs” of Vietnam being

the high-profile characters who were sentenced to death. The point, many

in Vietnam say, is to send a message.

Adam McCarty, chief economist with the Hanoi-based consulting firm

Mekong Economics, says that “It’s a message to those in this game to be

less greedy and that business as usual is getting out of hand.”

“The message to people in the system is this: Your chances of getting

caught are increasing,” McCarty continued. “Don’t just rely on big

people above you. Because some of these [perpetrators] would’ve had big

people above them. And it didn’t help them.”

“They don’t care about foreigners. It’s all internal politics,”

McCarty said. He explains that foreign banking learders wouldn’t be

dissuaded by a few executions anyway. “If you really want to want to

resolve the problem, you can’t just arrest people,” he said. “You’ve got

to improve accountability and transparency in the entire system.”

A local, Vietnames op-ed recently ran, confronting this issue, saying

that, “it is better to prevent corruption,” the paper opined, “than

deal with it after the fact.”

(Article by M.B. David)

A number of people have been inquiring about coins as an investment

for parking money. Keep in mind that the best market for coins or stamps

tend to be the country of origin. Thus, US coins will bring the highest

prices in the USA just as German will bring the best price in Germany.

There are some markets that are international. That is Art where in

the late 1980s, the Japanese began buying famous art at huge prices.

Ryoei Saito had purchased Vincent van Gogh’s: “Portrait of Doctor Gachet”, (1890) paying $82.5 million back in 1990

(Inflation adjusted price: $146,8 million). Note: Saito lost a fortune

in the Japanese Depression and the whereabouts of the painting are now

unknown).

Ancient Coins are in that same category where the market is truly

international. The biggest buyers these days are in China and Russia.

Many famous people collected Ancient Coins from President Teddy

Roosevelt but there was also the American coin collection of US

president John Quincy Adams, Many American billionaires also formed

famous Ancient Coin collections, notably J.P. Morgan, Calouste

Gulbenkian, William Randolph Hearst, J. Paul Getty, and Nelson Bunker

Hunt (whose collection was auctioned off by Sothebys shown above). King Farouk I of Egypt assembled a massive coin collection.

Perhaps the earliest known major collector was the Roman Emperor

Augustus. Nearly all of the great European national collections were

first formed privately by kings and nobility who were often avid

collectors. Lorenzo de’ Medici, the patron of the Renaissance, was one

of the most notable ancient coin collectors of his time. Even the

Catholic popes formed outstanding private collections which are now the

core of the current Vatican collections. And many important scientists

and scholars, such as Sigmund Freud and Desmond Morris, have also formed

fine collections. In our own time many famous personalities such as

Buddy Ebsen, Elton John and Tina Turner, to mention just a few, have

also been avid collectors. There were other collectors of stamps right

down to Calvin Klein.

The Ancient Coin market is international and way under priced

compared to US coins, but far broader in the scope of collectors coming

from truly around the world. There will be such a gathering at a show in

New York City come January. The US coin market holds the record for prices paid with a 1794 US Silver Dollar fetching more than $10 million (seek Stacks Bower Sale)..

The most expensive painting was the 2011 sale for $250 million of PAUL CÉZANNE“The Card Players”, 1892/93 (Inflation adjusted price: $258,4 million). Seller: George Embiricos. Buyer: Royal Family of Qatar.

The same trend is impacting art and collectibles.

Rare coins are

becoming rarer as those who have them just hold and the supply continues

to shrink. Every field is pretty much the same story. Nobody wants to

sell for then what do you do with the cash?

Many emails have come in asking if we can assist in obtaining

high-end ancient coins since they are an international item and movable

without tariffs. I realize this may be in many respects safer than just

metals and diamonds for transport. But I am not sure there is enough of a

supply even available of coins $10,000+. Most seem to go to auction

where they know they can get big bucks. Here is a Naxos tetradrachm,

probably the finest known that would probably bring $1 million+ today.

If there are any hoards that appear, I typically get a phone call.

We

will keep everyone in mind since so many are looking to get “off the grid” these days and ancient coins are not likely to be confiscated as was the case with gold..

WASHINGTON

(MarketWatch) ) — Former Federal Reserve Chairman Ben Bernanke believes

history has already vindicated the novel efforts of the U.S. central

bank to revive the economy after the financial crisis of 2008.

The

Fed and the Bank of England offered financial aid to beleaguered banks

and deployed tools such as quantitative easing — creating new money — on

a massive scale to help heal badly damaged economies.

The result

has been that the U.S. and Britain have grown much faster than the

European Union, whose response has been less aggressive.

‘By stabilizing the financial system, we avoided much,

much worse persistently bad consequences for our economies.’

“By stabilizing the

financial system, we avoided much, much worse, persistently bad

consequences for our economies,” Bernanke said in an interview

with Mervyn King on BBC. King was head of the Bank of England during

the crisis and was a constant ally of Bernanke, a longtime friend whom

he had first met at MIT three decades earlier.

Saturday, December 27, 2014

David Stockman Debunks TARP Profit Claims: The Fed Runs A ‘No Banker Left Behind’ Program

By John Morgan at NewsmaxFinance

Washington’s untruths about the Troubled Asset Relief Program

(TARP)’s so-called “success” add up to something worse than the original

taxpayer bailouts of big banks and other corporations, according to

David Stockman, White House budget chief during the Regan

administration.

He noted the Treasury Department recently concluded that the 2008

TARP had actually returned a profit of $15.3 billion, returning $441.7

billion on the $426.4 in taxpayer monies invested to save the likes of

Citigroup, Bank of America, General Motors, American International Group

(AIG) and other pre-meltdown spendthrifts.

“The ‘small profit’, along with most of the so-called ‘recovery’ of

Uncle Sam’s $426 billion initial investment, was ground out of the backs

of America’s savers and depositors; or it was scalped from the massive

financial bubbles the Fed has generated in the Wall Street casino,” Stockman wrote on his Contra Corner blog.

“In short, under an honest monetary regime of market clearing

interest rates, bank balance sheets would be far smaller. Likewise,

deposit costs would be far higher, and opportunities to scalp profits

from the global scramble for yield far less abundant.”

Stockman said the mainstream economics narrative and media coverage

on the Federal Reserve’s ultra-easy money policies is simply

perpetuating a fiction.

That’s because “what lies beneath its ‘extraordinary measures,’ such

as ZIRP [zero interest rate policy], QE [quantitative easing], wealth

effects and the rest of the litany, is a central banking regime that

systematically destroys savers. Period,” he claimed.

Stockman said the central bank’s ZIRP has allowed big banks to profit

while average Americans get squeezed by earning next to nothing on

their savings.

“The policy apparatus of the state has subjected savers to brutal

punishment for one reason alone. Namely, to enable the insolvent big

banks of America to dig their way out of the deep hole they were in at

the time of the financial crisis. By scalping false profits from the

Fed’s regime of financial repression, they have, in fact, been able to

return accounting profits to pre-crisis levels and beyond.”

He noted that ZIRP has enabled banks to carry $10 trillion of

deposits at negative real interest rates, while making money on that

cash, and pay out an average of 0.4 percent on six-month CDs when an

honest payout should be closer to 4.0 percent.

“This has been called the Fed’s ‘No Banker Left Behind’ program and for good reason,” Stockman said.

“But the heart of the matter is this. The Fed and other central banks

of the world have created trillions of fiat credit that is drastically

mispriced and would not even exist in a free market based on honest

savings from current production and legitimate requirements for capital

investment.

“TARP wasn’t ‘repaid’ with a profit. It was simply perpetuated and

morphed into a new form of destructive state subvention and

mal-investment.”

The Center for Economic and Policy Research

(CEPR) was likewise suspicious of the official government line that the

U.S. made a “profit” on its TARP taxpayer loans to corporate America,

and called The New York Times’ coverage of the matter a “children’s

story.”

“Before you start thinking that this is a great idea and we should

give all the government’s money to the Wall Street banks, imagine that

we had given the same money to a different institution, Bernie Madoff’s

investment fund. As we all know, Madoff’s fund was bankrupt at the time

because he was running it as a Ponzi, the new investors paid off the

earlier investors. He hadn’t made a penny on actual investment in

years,” said CEPR on its website.

CEPR said if the government had lent Madoff tens of billions of

dollars at the same low rates it charged Wall Street banks, Madoff

easily could have invested the money and paid off the debt, also. (It

apparently helps when taxpayers are subsidizing your loans.)

“This would have then allowed (former Treasury Secretary) Timothy

Geithner to boast about how we made a profit on the loans to Bernie

Madoff.

“The reality is that the boast of a profit in this context is pretty

damn silly. The question is whether an important public purpose was

served by rescuing the Wall Street banks from their own greed.”

Friday, December 26, 2014

Opinion: The Fed is heading for another catastrophe

With so much dry kindling, it will not take much to spark the next conflagration

By

StephenS. Roach

In these days of froth, the

persistence of extraordinary policy accommodation in a financial system

flooded with liquidity poses a great danger. Indeed, that could well be

the lesson of recent equity- and currency-market volatility and, of

course, plummeting oil prices.

With so much dry kindling, it will not take much to spark the next conflagration.

Central

banking has lost its way. Trapped in a post-crisis quagmire of zero

interest rates and swollen balance sheets, the world’s major central

banks do not have an effective strategy for regaining control over

financial markets or the real economies that they are supposed to

manage. Policy levers — both benchmark interest rates and central banks’

balance sheets — remain at their emergency settings, even though the

emergency ended long ago.

While this approach has

succeeded in boosting financial markets, it has failed to cure bruised

and battered developed economies, which remain mired in subpar

recoveries and plagued with deflationary risks. Moreover, the longer

central banks promote financial-market froth, the more dependent their

economies become on these precarious markets and the weaker the

incentives for politicians and fiscal authorities to address the need

for balance-sheet repair and structural reform.

A new approach is

needed. Central banks should normalize crisis-induced policies as soon

as possible. Financial markets will, of course, object loudly. But what

do independent central banks stand for if they are not prepared to face

up to the markets and make the tough and disciplined choices that

responsible economic stewardship demands?

The unprecedented financial

engineering by central banks over the last six years has been decisive

in setting asset prices in major markets worldwide. But now it is time

for the Fed and its counterparts elsewhere to abandon financial

engineering and begin marshaling the tools they will need to cope with

the inevitable next crisis. With zero interest rates and outsize balance

sheets, that is exactly what they are lacking.

There's only one media in the United States: it's all mainstream in that it's all owned by billionaires who all have the exact same motivation which is to protect their billions.

NBC, FOX, BLOOMBERG, CBS, NEW YORK TIMES, HERITAGE FOUNDATION, PROGRESSIVE POLICY INSTITUTE, SIRIUS, CNN, ETC: all owned or funded by billionaires, all perpetuate the same narrative: The US banking system is basically and fundamentally sound, profitable, deep, and safe.

This is the narrative that was shaken and almost crumbled in 2008. It was saved by the most massive transfer of wealth from the citizenry to the banking elite in the history of the world.

The narrative, now, is that the banking system is stronger than ever, that it didn't really even need the bailouts which were forced upon them and that they've paid it all back plus interest. And the economy is healing and quickly returning to full strength.

Who reported on the destruction of the Volker rule? The story was annihilated by the "story" that Sony Pictures didn't open a slapstick comedy on time because of "hackers." Wow. That's so much more important than the fact that banks again have been licensed to be gambling parlors.

Meanwhile the banks have dismantled Dodd Frank, jetisoned the Volker Rule and are piling up bets in derivatives that leverage their balance sheets by 50-1. The Fed is in worse shape with over 3 Trillion dollars of bad debt on their balance sheet.

As long is the "Strong Bank" narrative is believed by most of the people, Gold will languish. It may fall to 1000 or even 900 dollars an ounce. Which is still 300 percent above where it started to move when people began to doubt the efficacy of the banking system back in 2000.

But the very second the narrative cracks and doubt spreads through the mass consciousness gold will move at the speed of thought.

And it won't have anything to do with COT reports or calls for delivery on the Comex, or Diwali, or Chinese New Year.

It will be 400,000,000 Americans and 4 Billion other world citizens suddenly realizing all at once that their dollars and their euros and their yen in their Bank Accounts are not a safe store of value.

New G20 Rules: Cyprus-style Bail-ins to Hit Depositors AND Pensioners

by Ellen Hodgson Brown / December 1st, 2014

On the weekend of November 16th, the G20 leaders whisked into

Brisbane, posed for their photo ops, approved some proposals, made a

show of roundly disapproving of Russian President Vladimir Putin, and

whisked out again. It was all so fast, they may not have known what they

were endorsing when they rubber-stamped the Financial Stability Board’s

“Adequacy of Loss-Absorbing Capacity of Global Systemically Important

Banks in Resolution,” which completely changes the rules of banking.

Russell Napier, writing in ZeroHedge,

called it “the day money died.” In any case, it may have been the day

deposits died as money. Unlike coins and paper bills, which cannot be

written down or given a “haircut,” says Napier, deposits are now “just

part of commercial banks’ capital structure.” That means they can be

“bailed in” or confiscated to save the megabanks from derivative bets

gone wrong.

On December 11, 2014, the US House passed a bill

repealing the Dodd-Frank requirement that risky derivatives be pushed

into big-bank subsidiaries, leaving our deposits and pensions exposed to

massive derivatives losses. The bill was vigorously challenged by

Senator Elizabeth Warren; but the tide turned when Jamie Dimon, CEO of

JPMorganChase, stepped into the ring. Perhaps what prompted his

intervention was the unanticipated $40 drop in the price of oil. As financial blogger Michael Snyder points out,

that drop could trigger a derivatives payout that could bankrupt the

biggest banks. And if the G20’s new “bail-in” rules are formalized,

depositors and pensioners could be on the hook.

The new bail-in rules were discussed in my last post here.

They are edicts of the Financial Stability Board (FSB), an unelected

body of central bankers and finance ministers headquartered in the Bank

for International Settlements in Basel,

Fed Delays Volcker Rule, Giving Wall Street Another Holiday Gift

WASHINGTON -- Christmas came early for Wall Street this year. The Federal Reserve on Thursday granted

banks an extra year to comply with a key provision of the Volcker Rule,

a move that gives financial lobbyists more time to kill the new

regulation before it goes into effect.

The Volcker Rule is a key

element of the 2010 Dodd-Frank financial reform law that bans banks from

engaging in proprietary trading -- speculative deals that are designed

only to benefit the bank itself, rather than its clients. Thursday's

move by the Fed gives banks an additional year to unwind investments in

private equity firms, hedge funds and specialty securities projects. The

central bank also said it plans to extend the deadline by another 12

months next year, which would give Wall Street a two-year reprieve

through the 2016 presidential election.

The Fed's delay comes less

than a week after Congress granted Wall Street a reprieve from another

reform that had been mandated by the 2010 Dodd-Frank financial reform

law. The measure, known as the swaps push-out rule had eliminated

federal subsidies for trading in risky derivatives -- the complex

contracts at the heart of the 2008 banking meltdown. Bank watchdogs say

the Volcker Rule delay adds insult to injury.

A HIGHLY IMPORTANT IMPERIAL EMBROIDERED SILK THANGKA

YONGLE SIX-CHARACTER PRESENTATION MARK AND OF THE PERIOD (1402-1424)

This massive panel is exquisitely embroidered in gold thread and brilliant coloured silk threads on leaf-green jiang chou

silk enriched with a regular pattern of dark blue medallions of curled

leafy scrolls outlined with gold thread. The central image is of the

wrathful Raktayamari, depicted in tones of red, standing in yab-yum embracing his consort Vajravetali. Her left leg encircling his waist, his right hand wielding above his head a khatvanga embellished with human heads in varying states and the vajra thunderbolt, his left arm supporting his facing consort and holding a kapala

or skull cap in his left hand. The locked couple is trampling on the

blue corpse of Yama, the Lord of death, wearing a tiger skin and crown,

lying on the back of their mount, a brown buffalo recumbent on a

multi-coloured lotus base. All below two rows of buddhas and

bodhisattvas seated on lotus bases, the upper including Heruka

Vajrabhairava on the far left and Manjusri on the far right, flanking

the five Dhyani Buddhas, Ratnasambhava, Akshobhya, Vairocana, Amitabha

and Amoghasiddhi. The lower row with Green Tara and White Tara. On the

lower panel is a row of seven offering goddesses dancing on lotus bases

and holding aloft dishes as offerings below the couple. The thangka is bordered by an embroidered yellow-ground band of vajra.

On the upper right side is the vertical presentation mark in gold

thread on a red embroidered ground below the White Tara. Accompanied

with a Qing dynasty silk surround now detached.

$565,000 Greubel Forsey GMT Black Watch Is Idiosyncratic, Incredible(y stupid)

By Stephen PulvirentDec 14, 2014 1:03 AM ET

Photographer: Stephen Pulvirent/Bloomberg

The Greubel Forsey GMT Black.

There are no two ways about it: Greubel Forsey makes incredible

watches. The designs are a bit, shall we say, "idiosyncratic," and after

a decade they still continue to ignore all but the highest end of the

market. It's all part of the charm. The GMT was first released in 2011,

but the GMT Black is a departure from the rose gold and platinum

versions we've seen trickle out since, utilizing lightweight titanium

instead of a precious metal for the case. This is a watch to stare at.

Go ahead, we'll be here a while. First Thoughts:

Even if the GMT Black isn't the sort of thing I'd wear to watch to the

Giants game on Sunday (unless I owned the team, maybe), it's the most

approachable version of one of the most impressive watches on the

market. The titanium case means that even with its large profile it

still weighs less than a Ferrari -- even if it costs more. The black

finish makes it less in-your-face and lets you really admire the

finishing on the non-blackened components. The GMT might be a few years

old by now, but staring at that globe never gets old. Cocktail Party Fact: It's

a little hard to give Greubel Forsey's case shapes proper names, but

that wonky geometry has a purpose. At 43.5mm across (without the

bulges), the GMT's case is already big. The idea with the asymmetrical

design is to highlight the design elements that Greubel Forsey wants

wearers to focus on, to give the tourbillon and globe room to breathe,

without having a bunch of empty dial space around the edges. The extra

sapphire window at the side of the globe is another nice touch that adds

to the effect. It might seem strange at first, but the unusual shape is

a really smart solution.

Shakespeare's First Folio found in France: Bard's 400-year-old book

was overlooked on library shelf - and it's worth £3.5 million

Found in St-Omer, the book is the first compilation of the Bard's plays

Book is the 231st copy found in the world, and only the second in France

Because it is in English, it is thought French readers overlooked it

It is in good condition, but missing 30 pages, including the title page

First folio is the only source for 18 of Bard's plays, including Macbeth

Published seven years after Shakespeare's death, it originally sold for £1

A

rare and valuable copy of William Shakespeare's First Folio - the

first-ever compilation of the Bard's plays - has been uncovered in a

provincial library in France.

The

1623 book, which is one of the most coveted in the world, lay

undiscovered among hundreds of others in St-Omer, near Calais, for some

400 years.

Worth

up to £3.5 million ($5.5 million), it was discovered when librarian

Remy Cordonnier dusted off a book of Shakespeare's works for an

exhibition.

+8

Hidden in plain sight: A rare and valuable copy of William Shakespeare's First Folio (pictured), the fir

Jamie Dimon, head of JP Morgan, personally telephoned individual

lawmakers to urge them to vote for the repeal of Dodd Frank. This is

getting really out of hand. Let us make this very clear. Besides the

fact that these banks LACK the models to prevent them

from blowing up every single time running to government with their hand

out asking can they spare a trillion, the sheer fact that they can make

heaps of money from trading means they are NOT lending.

Spain converted itself from the richest nation in Europe to the poorest

by doing precisely this short-term type planning.

Spain did not invest in developing its country. Spain squandered all

its money living high on the hog, as they say. The saying was a French

man knew how to unload ships rather than a Spaniard. The banks are

traders not lenders.They are trading with YOUR money.

Profits are their’s – losses are taxpayers. Allowing them to be

derivative junkies means they do not do what they are supposed to be

doing – lending money that expands jobs and builds the national economy.

The Republicans are simply counting their donations for political

campaigns. This will be the downfall of the Republican Party come 2016.

The banks will blow up AS ALWAYS, and the people will

get outraged because at G20 they said the depositor has to pay for the

next bailout – bail-ins. There is no disclosure mandated. There should

be a warning label on bank accounts – THIS BANK SPECULATES WITH YOUR MONEY. Hey – borrow this regulation from the FDA regulating food

The Department of Treasury is spending $200,000 on survival kits for all of its employees who oversee the federal banking system, according to a new solicitation. As FreeBeacon reports, survival kits will be delivered to every major bank in the United States and includes a solar blanket, food bar, water-purification tablets, and dust mask (among other things). The question, obviously, is just what do they know that the rest of us don't? As Free Beacon reports,

The Department of Treasury is seeking to order survival kits for all of its employees who oversee the federal banking system, according to a new solicitation.

The emergency supplies would be for every employee at the

Office of the Comptroller of the Currency (OCC), which conducts on-site

reviews of banks throughout the country. The survival kit includes everything from water purification tablets to solar blankets.

The government is willing to spend up to $200,000 on the kits, according to the solicitation released on Dec. 4.

The survival kits must come in a fanny-pack or backpack that can fit

all of the items, including a 33-piece personal first aid kit with

“decongestant tablets,” a variety of bandages, and medicines.

After months of hard-fought negotiations over agency dollars and

policy provisions, the net result is a 1,600 page bill released last

night.The deal was announced late yesterday after Democrats accepted

Republican demands to undo

some regulations including the banking provision that will allow the

trading banks to deal in derivatives again in subsidiaries will full

insurance from the government once again. The big banks can keep swaps

trading in units with federal FDIC insurance. Just amazing. Grease

enough palms and the country is yours. This bill has to pass by Friday.

They would not have stuck this partial repeal of Dodd-Frank if they did

not have the votes.

Big Banks Will Take Depositors Money In Next Crash -Ellen Brown

The G-20 met recently in Australia to make new banking rules for the

next financial calamity. Financial reform advocate Ellen Brown says

these new rules will allow banks to take money from depositors and

pensioners globally. Brown explains, “It became rules we agreed to

actually implement. There was no treaty, and Congress didn’t agree to

all this. They use words so that it’s not obvious to tell what they

have done, but what they did was say, basically, that we, the

governments, are no longer going to be responsible for bailing out the

big banks. These are about 30 international banks. So, you are

going to have to save yourselves, and the way you are going to have to

do it is by bailing in the money of your creditors. The largest class

of creditors of any bank is the depositors.”

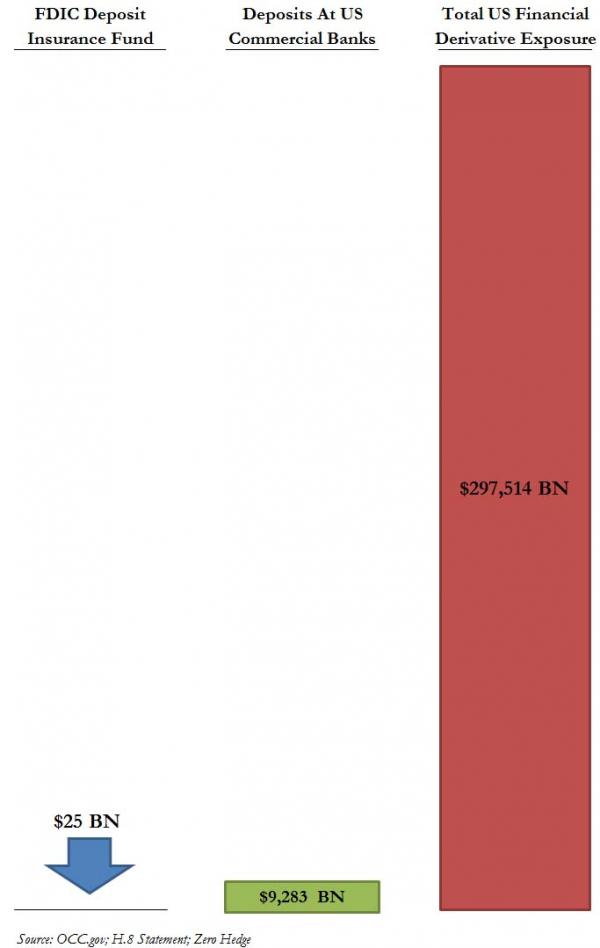

It gets worse, as Brown goes on to say,

“Theoretically, we are protected by deposit insurance up to $250,000 in

the U.S. and 100,000 euros in Europe. The FDIC fund has $46 billion,

the last time I looked, to cover $4.5 trillion worth of deposits. There

is also $280 trillion worth of derivatives that the five biggest banks

in the U.S. are exposed to, and under the bankruptcy reform act of 2005,

derivatives go first. So, they are basically exempt from these new

rules. They just snatch the collateral. So, if you had a big

derivatives bust that brought down JP Morgan or Bank of America, there

is no way there is going to be collateral left for the FDIC or for the

secured depositors. This would include state and local governments.

They all put their money in these big banks. So, even though we are

protected by the FDIC, the FDIC is not going to have the money. . . . This

makes it legal for these big 30 banks to take our money when they

become insolvent. They are too-big-to-fail. This was supposed to avoid

too-big-to-fail, but what it does is institutionalizes

too-big-to-fail. They are not going to go down. They are going to take

our money instead.”

Part of the coming financial calamity will involve hundreds of

trillions of dollars in un-backed derivatives. Brown contends, “If the

derivative bubble pops, nobody knows what is going to happen, and it’s

obvious it has to pop. It can’t just keep growing. Depending on who

you read, some people say it is up to two quadrillion dollars. It’s

virtual money, and it cannot keep going on.”

When a financial crash does happen, you can forget about getting

immediate access to your money. Brown says, “The banks will say, well,

we don’t have it. All the money goes into one big pool since Glass

Steagall was repealed. They are allowed to gamble with that money and

that’s what they do. I think maybe Bank of America is the most

vulnerable because of Merrill Lynch. Everybody is concerned, and they

do very risky deals and they are on the edge. I think they have over

$50 trillion in derivatives and over $1 trillion in deposits. . . The

Dodd-Frank Act says we, the people, are no longer going to be

responsible for the big banks when they collapse. It is not clear the

FDIC will even be able to borrow from the Treasury, but even if they

could, who is going to pay that money back? Let’s say they borrowed $1

trillion. Who is going to pay that $1 trillion back? It will bankrupt

all the small banks that had to contribute to this premium. They will

say we’re raising your premium to everything you got, basically. Little

banks will go out of business, and who is going to survive–the big

banks. . . . What we’re going to have left is five big banks, and

everybody else is going to be bankrupt.”

The high-flying banks are at it again. There has been lobbying going

on to sneak a clause in the continuing resolution to fund the government

over the holidays for the December 11th deadline. The provision they

are trying to sneak in would allow the banks to trade derivatives

through subsidiaries that are federally insured by the FDIC. In other

words, they are circumventing the very reforms of the 2007-2009 crash.

This is not yet confirmed. The bill was held up and the final

language was being submitted at midnight last night. This is how they

operate so everyone is asleep and the real dirty shit is stuffed in

bills in the middle of the night. This tactic is outright fraud upon the

nation and the world. We seriously need political reform or there will

be no future.

This is how the lame-duck Congress always functions – bribe time on

steroids. The manipulating banks are trying to sneak this into a bill

to keep the government funded for Christmas and they know they will get

the votes because nobody will read the fine print on Capitol Hill. They

are trying to now effectively repeal the Dodd–Frank Wall Street Reform and Consumer Protection Act (Pub.L. 111–203, H.R. 4173)

before the new Congress comes in. These lame-duck sessions are highly

dangerous and have done far more long-term damage to the nation than any

other session. This is Congress on sale to the highest bidder.

When we get the real real final language, we will confirm everyone what they have pulled off this time if it survives.

On the weekend of November 16th, the G20 leaders

whisked into Brisbane, posed for their photo ops, approved some

proposals, made a show of roundly disapproving of Russian President

Vladimir Putin, and whisked out again. It was all so fast, they may not

have known what they were endorsing when they rubber-stamped the

Financial Stability Board’s “Adequacy of Loss-Absorbing Capacity of

Global Systemically Important Banks in Resolution,” which completely

changes the rules of banking. Russell Napier, writing in ZeroHedge,

called it “the day money died.” In any case, it may have been the day

deposits died as money. Unlike coins and paper bills, which cannot be

written down or given a “haircut,” says Napier, deposits are now “just

part of commercial banks’ capital structure.” That means they can be

“bailed in” or confiscated to save the megabanks from derivative bets

gone wrong.

Rather than reining in the massive and risky derivatives casino, the new rules prioritize the payment of banks’ derivatives obligations to each other,

ahead of everyone else. That includes not only depositors, public and

private, but the pension funds that are the target market for the latest

bail-in play, called “bail-inable” bonds.

“Bail in” has been sold as avoiding future government bailouts and

eliminating too big to fail (TBTF). But it actually institutionalizes

TBTF, since the big banks are kept in business by expropriating the

funds of their creditors.

It is a neat solution for bankers and politicians, who don’t want to

have to deal with another messy banking crisis and are happy to see it

disposed of by statute. But a bail-in could have worse consequences than

a bailout for the public. If your taxes go up, you will probably still

be able to pay the bills. If your bank account or pension gets wiped

out, you could wind up in the street or sharing food with your pets.

In theory, US deposits under $250,000 are protected by federal

deposit insurance; but deposit insurance funds in both the US and Europe

are woefully underfunded, particularly when derivative claims are

factored in. The problem is graphically illustrated in this chart from a March 2013 ZeroHedge post:

Tuesday, December 2, 2014

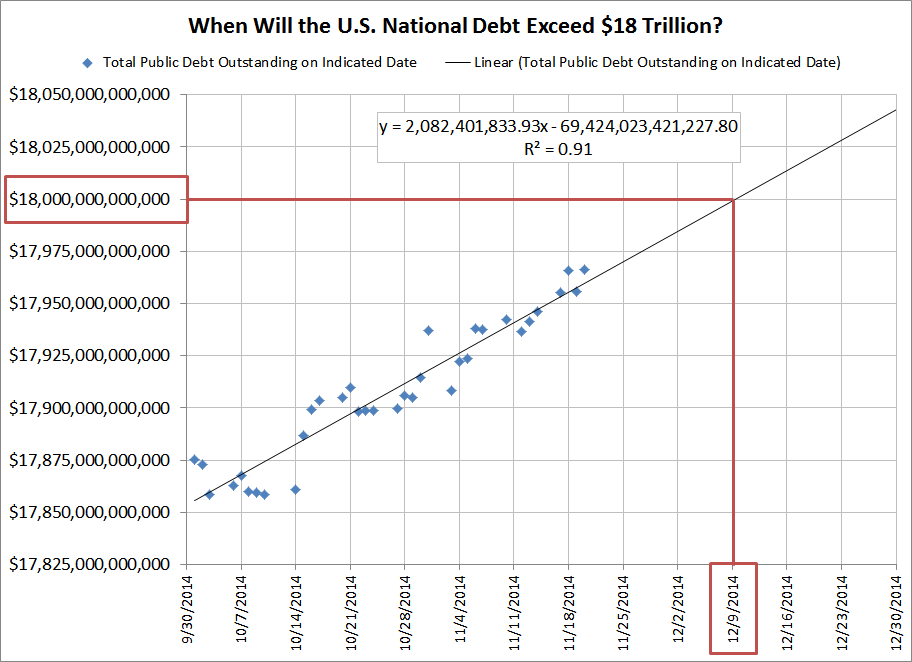

Chart Of The Day: US Public Debt Will Hit $18 Trillion On December 9th

By Craig Eyermann at MyGovCost.org

Sometime in the next two to three weeks, the total public debt outstanding

for the U.S. government will exceed 18 trillion dollars. If you were to

ask us to pin down a precise date, we would say sometime around

December 9, 2014, given the rate at which the national debt has been

increasing during the federal government’s current fiscal year:

Since the start of the U.S. federal government’s 2015 fiscal year on

October 1, 2014, the national debt has grown at an average rate of $2.08

billion per day.

If it helps put these very large numbers into a more human scale,

when the U.S. national debt reaches $18 trillion, that will work out to

be about $124,275 per U.S. household, which is up from $81,984 per U.S.

household at the end of the 2008 fiscal year. And the new figure would

be on top of your mortgage, car loans, student loans, credit cards, et cetera that you might also have.

But unlike those tangible things, where you can at least point to

your house, your car, your education, or even the Christmas presents you

might be buying this upcoming Black Friday, can you point to what you

personally got in return for that $42,291 worth of additional debt per

household that the federal government accumulated during the last six

years?

If you cannot, is it really worth it?

Getty Images

Getty Images